How Wealthy Individuals Use Charitable Trusts for Tax Efficiency

Charitable Trust Tax Efficiency Calculator

Enter your asset details below to see how different charitable strategies impact your taxes and cash flow.

You’ve probably heard the phrase "the rich don’t pay taxes." It’s a headline that sells newspapers and fuels political debates. But what does it actually mean? It rarely means breaking the law. Instead, it refers to a sophisticated use of legal structures-primarily charitable trusts-that allow high-net-worth individuals to defer, reduce, or eliminate taxes on their wealth while supporting causes they care about.

For most people, income tax is paid on money earned from wages. For the wealthy, however, the majority of income comes from capital gains-the increase in value of assets like stocks, real estate, and businesses. This distinction is crucial. When you sell an asset that has grown significantly, you owe capital gains tax. If you hold onto it until death, that tax might never be paid by the original owner, thanks to a rule called step-up in basis. But if you want to move that wealth now, without triggering a massive tax bill, charitable vehicles become essential tools.

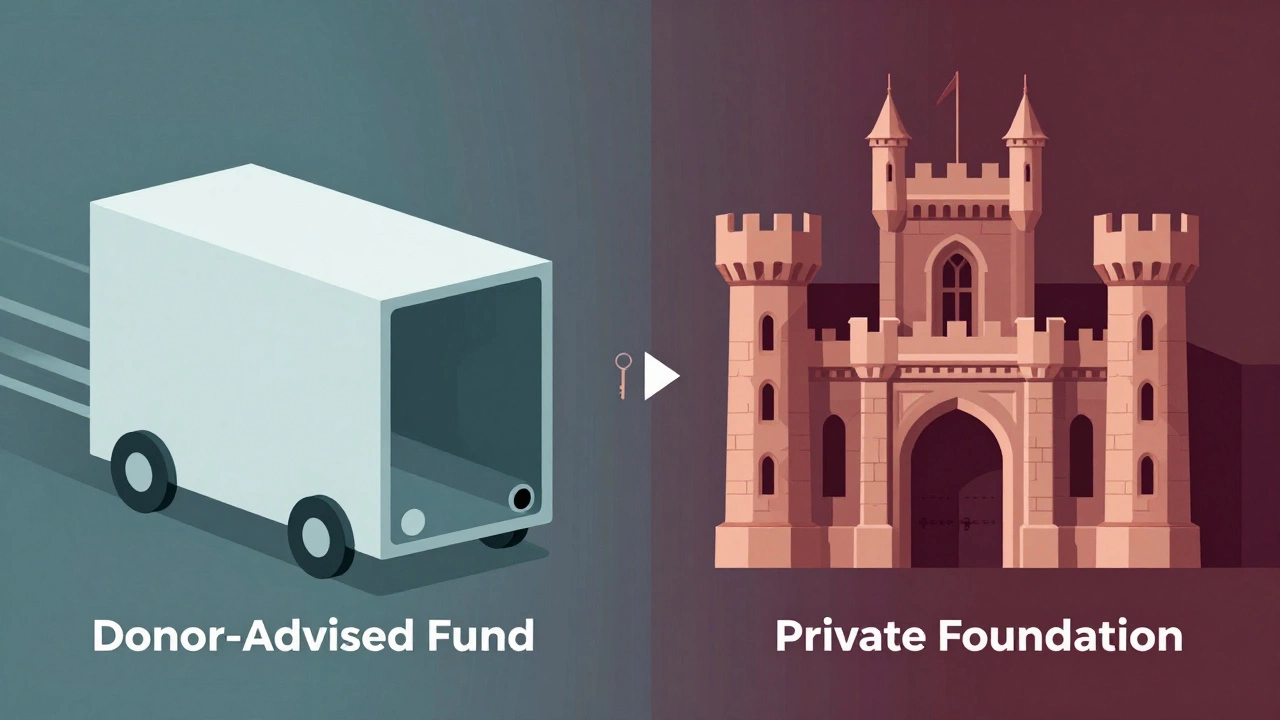

The Mechanics of the Donor-Advised Fund (DAF)

The most common entry point for this strategy is the Donor-Advised Fund, or DAF. Think of a DAF as a personal grant-making account managed by a public charity. You contribute cash or appreciated assets to the fund, receive an immediate tax deduction for the full fair market value, and then recommend grants to other charities over time.

Here is why this matters: Suppose you own shares in a company that you bought for $10,000 years ago. Today, those shares are worth $1 million. If you sell them, you’ll owe roughly 20% to 37% in federal capital gains tax, plus potentially 3.8% in net investment income tax. That’s a huge hit before you even think about donating.

Instead, you donate the shares directly to your DAF. The DAF sells the shares tax-free because it is a tax-exempt organization. You get a $1 million deduction on your current year’s tax return, lowering your taxable income significantly. Meanwhile, the $1 million sits in the DAF, investing and growing tax-free. You can then distribute that money to charities at your own pace, perhaps over the next decade. You’ve avoided the capital gains tax entirely, reduced your current income tax, and kept control over where the money goes.

- Immediate Deduction: You claim the tax break in the year you contribute, even if the money isn’t distributed to charities yet.

- No Capital Gains Tax: Appreciated assets avoid the 20-37% hit upon sale within the fund.

- Tax-Free Growth: Investments inside the DAF grow without being taxed annually.

- Simplicity: Unlike foundations, DAFs have minimal administrative costs and no annual filing requirements for the donor.

Private Foundations: Control vs. Cost

If a DAF is the quick-and-easy option, a Private Foundation is the heavy-duty vehicle. A private foundation is its own separate legal entity, usually structured as a non-profit corporation. It offers more control and prestige but comes with higher costs and stricter regulations.

Wealthy families often choose private foundations when they want to establish a lasting legacy under their family name. Unlike a DAF, which is administered by a sponsor organization (like Fidelity or Vanguard), a private foundation requires its own board of directors, typically family members. This allows for direct involvement in selecting grantees and managing investments.

However, the trade-offs are significant. Private foundations must distribute at least 5% of their net asset value annually for charitable purposes. They face higher excise taxes on investment income (1% to 2%) compared to the 0% for DAFs. They also require annual Form 990-PF filings with the IRS, which are publicly available. This transparency can be a downside for donors who prefer privacy. Additionally, setting up and maintaining a private foundation costs thousands of dollars per year in legal and accounting fees.

| Feature | Donor-Advised Fund (DAF) | Private Foundation |

|---|---|---|

| Setup Cost | Low ($0 - $100) | High ($2,000 - $10,000+) |

| Annual Maintenance | Minimal (admin fee) | Significant (legal/accounting) |

| Distribution Requirement | None (donor decides) | Minimum 5% of assets/year |

| Control Level | Moderate (recommendations only) | High (board makes decisions) |

| Privacy | High (grants not public) | Low (Form 990-PF is public) |

| Best For | Bunching deductions, simplicity | Family legacy, long-term control |

The Split-Dollar Life Insurance Strategy

One of the more complex-and controversial-methods involves combining charitable giving with life insurance. This is often referred to as a split-dollar arrangement or using a Life Insurance Trust paired with a charitable gift.

In some variations, a donor contributes to a charitable remainder trust (CRT) or similar vehicle, which then uses the funds to purchase life insurance policies. The idea is to leverage the tax benefits of the charitable contribution while preserving wealth for heirs through the death benefit of the insurance policy. However, the IRS has cracked down heavily on abusive versions of these schemes. Recent legislation, such as the SECURE Act 2.0 passed in late 2022, eliminated certain tax breaks for split-dollar arrangements involving charitable gifts made after December 31, 2022.

Despite these restrictions, legitimate variations still exist for ultra-high-net-worth individuals. These strategies require meticulous planning by top-tier tax attorneys and actuaries. The goal is always the same: maximize the present value of the charitable deduction while minimizing the transfer of taxable assets out of the estate.

Charitable Remainder Trusts (CRTs): Income Now, Charity Later

A Charitable Remainder Trust flips the script on the DAF. Instead of donating now and getting a deduction later, you put assets into a CRT, and the trust pays *you* an income stream for a set period or for life. After that period ends, the remaining assets go to charity.

This is particularly useful for someone who owns a highly appreciated asset but needs current income. Let’s say you have a commercial building worth $5 million that generates rental income. If you sell it, you pay capital gains tax. If you donate it to a CRT, the trust sells it tax-free. The trust then invests the proceeds and pays you a guaranteed annuity or percentage of the trust’s value each year. At the end of your life (or a term of years, max 20), whatever is left goes to your chosen charity.

You get three things: 1. An immediate income tax deduction based on the present value of the charitable remainder. 2. No capital gains tax on the sale of the asset. 3. A steady income stream during your lifetime.

CRTs are complex and expensive to set up, often costing $10,000 or more in legal fees. They also come with strict rules about how much income you can take versus how much must remain for charity. If you take too much, the IRS may disallow the deduction. Therefore, actuarial tables are used to calculate the exact payout rates.

Estate Planning and Step-Up in Basis

It’s impossible to discuss wealthy tax strategies without mentioning the step-up in basis. Under current U.S. tax law, when you die, the cost basis of your assets is "stepped up" to their current market value. This means your heirs inherit the assets with zero capital gains tax liability if they sell immediately.

Many wealthy individuals simply hold their assets until death. They donate appreciated stock to a DAF or foundation in their final years to offset any income tax owed that year, or they leave the bulk of their portfolio to a private foundation. The foundation then sells the assets tax-free and distributes them to charities. The donor gets the tax deduction (on their final estate tax return, potentially reducing estate taxes), and the charities get the full value of the assets.

This strategy highlights a key difference between income tax and estate tax. While income tax is paid annually, estate tax is a one-time event. By using charitable trusts, donors can reduce the size of their taxable estate, thereby lowering or eliminating estate taxes, which can reach 40% for amounts above the exemption threshold (approximately $13.61 million per person in 2024, indexed for inflation).

Is It Legal? Yes. Is It Fair? Debatable.

All the strategies mentioned above are fully legal. They are built into the Internal Revenue Code to encourage philanthropy. The government wants people to give to charity, so it offers tax incentives to do so. The problem arises when the primary motivation becomes tax avoidance rather than genuine charitable impact.

Critics argue that these mechanisms allow the wealthy to retain too much control over their donations. With a DAF, you can donate millions today, get the tax break, and let the money sit there for decades, making no actual grants to help anyone in need. This is known as "bunching"-donating several years’ worth of planned gifts in a single year to exceed the standard deduction and maximize itemized deductions.

Proponents counter that this flexibility encourages larger donations than would otherwise occur. If you couldn’t deduct the full value of appreciated stock, many donors would just keep the stock and give less, or not at all. The system works because it aligns self-interest (tax savings) with social good (charitable funding).

Key Takeaways for High-Net-Worth Individuals

If you are considering these strategies, here are the critical steps: 1. Start Early: Charitable trusts take time to set up and fund. Waiting until the last minute can lead to missed opportunities or errors. 2. Consult Experts: Do not attempt this alone. You need a team including a CPA, an estate planning attorney, and a financial advisor who specializes in philanthropy. 3. Define Your Goals: Are you looking for immediate tax relief? Long-term family legacy? Privacy? Your goals will determine whether a DAF, private foundation, or CRT is right for you. 4. Understand the Rules: Each vehicle has specific distribution requirements and prohibited activities (e.g., self-dealing). Violating these can result in severe penalties. 5. Consider Impact: Ensure that your tax strategy doesn’t overshadow your charitable mission. The best plans balance financial efficiency with meaningful social impact.

Can I deduct more than my adjusted gross income (AGI) with a charitable trust?

Yes, but with limitations. For cash contributions to public charities, you can generally deduct up to 60% of your AGI. For appreciated assets, the limit is usually 30% of AGI. Any amount exceeding these limits can be carried forward for up to five years. This carryforward feature is powerful for "bunching" donations.

What is the minimum amount needed to start a Donor-Advised Fund?

There is no federal minimum, but sponsoring organizations set their own thresholds. Most major providers like Fidelity, Schwab, and Vanguard require initial contributions between $5,000 and $25,000. Some specialized firms may accept lower amounts, but the administrative costs make small balances inefficient.

Do I have to distribute money from my DAF every year?

No. Unlike private foundations, DAFs have no mandatory annual distribution requirement. You can contribute large sums, take the tax deduction, and let the funds grow tax-free for years or even decades before recommending any grants. This lack of pressure is a major advantage for strategic planning.

Can I name myself as a beneficiary of a charitable trust?

Generally, no. Charitable trusts must provide a substantial benefit to charity. In a Charitable Remainder Trust, you can receive income for life, but the remainder must go to charity. In a DAF or Private Foundation, you cannot benefit personally from the distributions. Doing so constitutes "self-dealing" and results in heavy IRS penalties.

How does the SECURE Act 2.0 affect charitable giving strategies?

The SECURE Act 2.0, enacted in December 2022, closed several loopholes. It eliminated the tax exclusion for charitable contributions made via IRA transfers after age 70½ if the donor receives anything in return (like life insurance benefits). It also restricted certain split-dollar life insurance arrangements linked to charitable gifts. Always consult a tax professional for post-2022 compliance.